Newsletter

|

Feb 7, 2025

Gaming will be responsible for kicking off the next wave of consumer investing

Copy Link

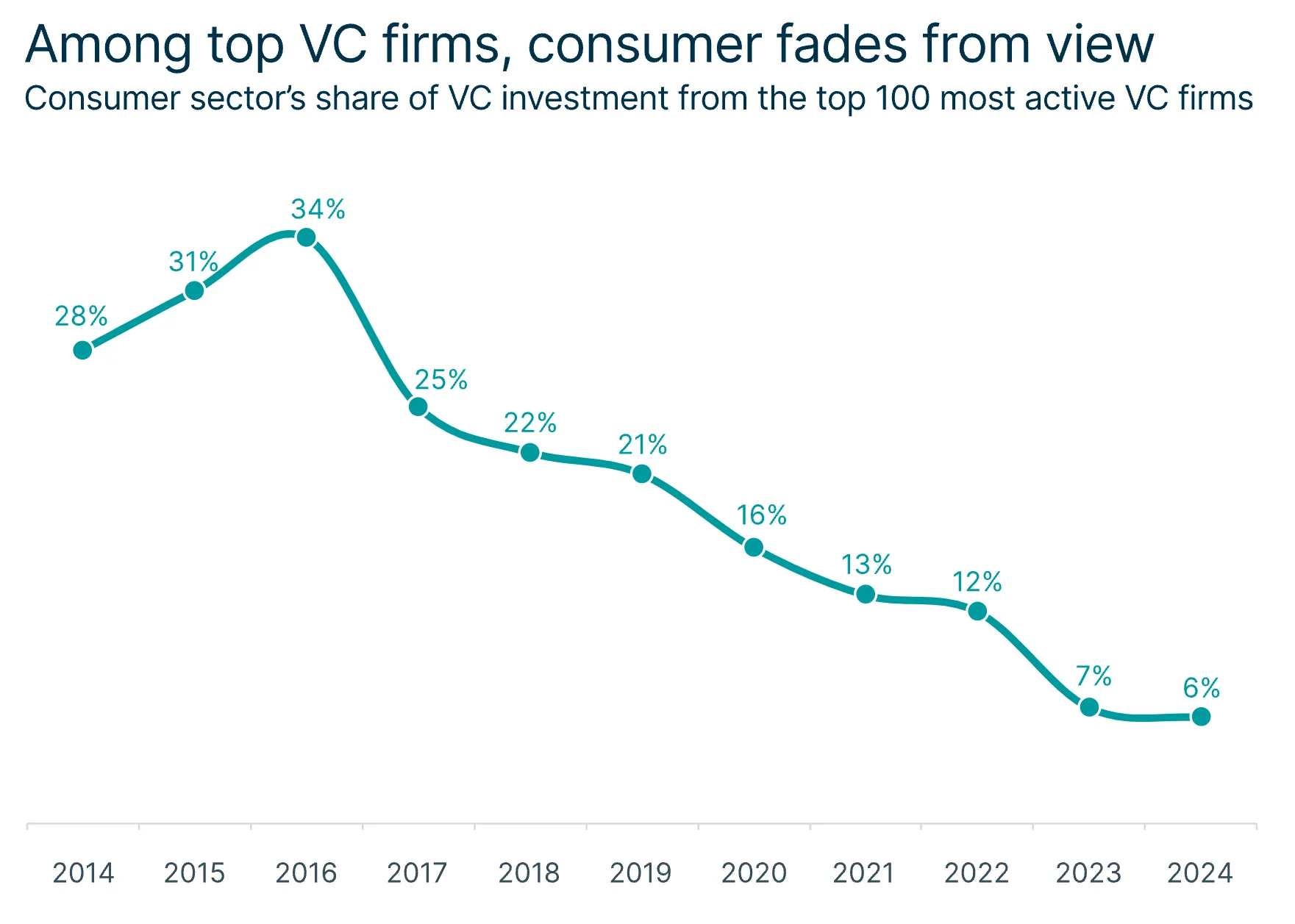

Over the past decade, venture capital firms have increasingly shifted away from investing in the consumer sector. In 2024, only 6% of all VC investment dollars went into the consumer sector from the top 100 most active VC firms (see chart above from SVB).

Thinking about the last 5+ years (setting game titles aside), the last great consumer app that truly has taken off in mass adoption has been ChatGPT. Before that, a few others worth highlighting were TikTok (2016), Discord (2015), Robinhood (2013), Coinbase (2012), Snapchat (2011), Instagram (2010), WhatsApp (2009), Uber (2009), Spotify (2008), Zillow (2006), and the list goes on. Many of these are Forever Apps (which we did a deep dive on in 2023) or short-term apps, which are also very lucrative consumer investments.

It has been a while since there was a steady release of new consumer apps/platforms that are capturing attention and mass adoption. We believe that the under investment from the venture capital space has partially contributed to that; and therein lies the opportunity.

Here are a few of the core factors that we believe have contributed to the slowdown in consumer investing from the venture capital investment firms:

Given the headwinds above (either real or perceived), it is understandable that the venture capital firms have quickly steered clear of the consumer category. That said, we at Konvoy believe that this presents a lucrative and opportunistic time to invest in the category alongside great operators who are innovating around the established incumbents.

Gaming is 21% of Consumer Unicorns Enterprise Value

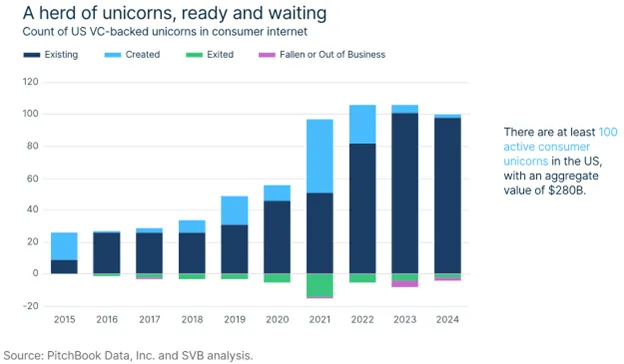

In the chart below from SVB, you will notice that there are ~100 active unicorns in the United States that are VC-backed in the consumer internet space. The number of consumer unicorns saw a large uptick in 2019 and then an unprecedented acceleration in 2021 on the back of low interest rates, high valuations, and a vibrant IPO market. In the US alone, there were 1,035 IPOs (highest ever, SPACs were 60% of these) that raised over $300 billion. Late stage VCs, growth equity, and cross-over hedge funds were extremely active.

However, the percentage of VC dollars investing in the consumer space fell rapidly from 21% (2019) to 13% (2021) over a 24-month period. Even since 2021, it has fallen from 13% to 6% in 2024, showcasing how the category has continued to fall out of favor.

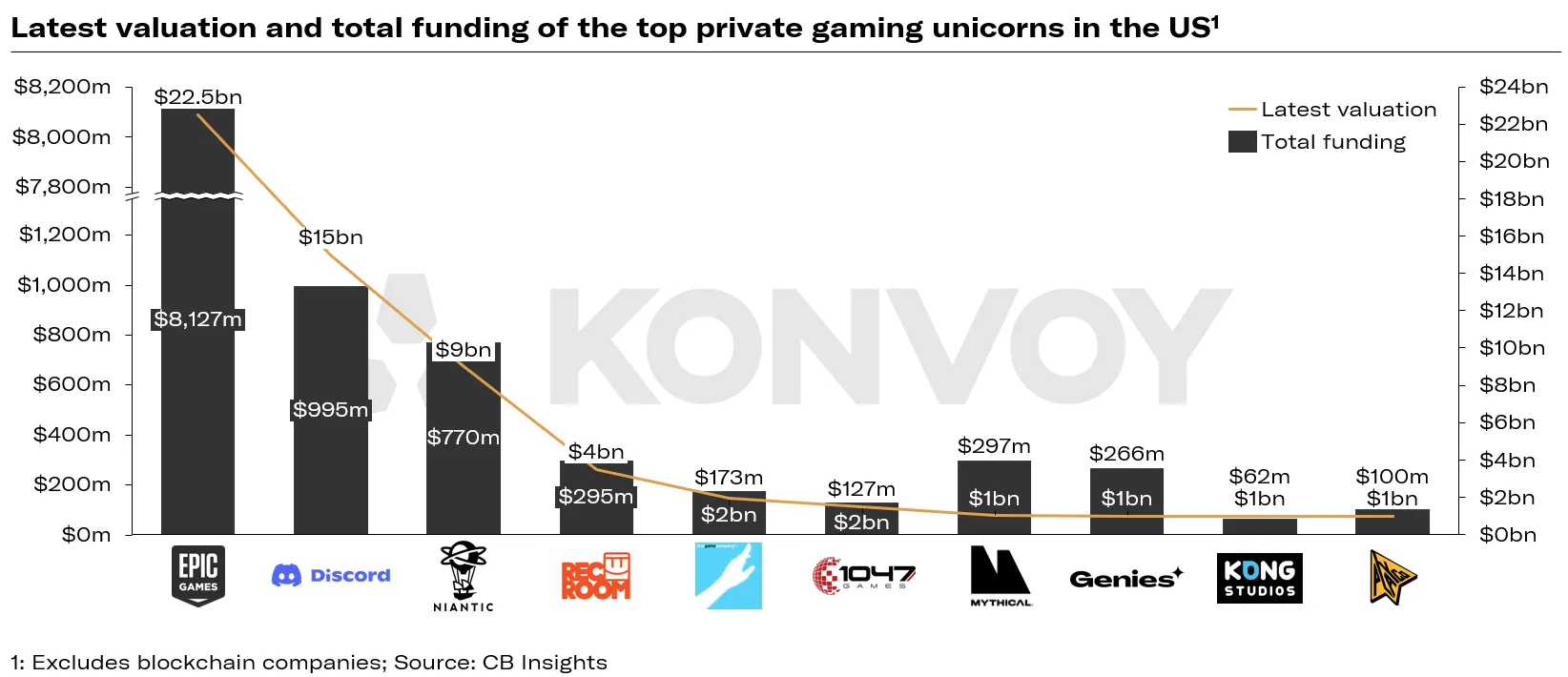

In gaming, there are 10 active unicorns that are based in the US. The full list below have raised a total of $12.1 billion since inception and their combined enterprise value (based on their last publicly announced valuation) is $60.3bn:

Only looking at the United States, these 10 gaming unicorns make up 10% of the 100 US consumer unicorns yet command ~21% ($57bn) of the total enterprise value ($280bn) of the US consumer internet unicorns. We believe that many on this list of 10 US gaming unicorns are very well positioned for liquidity events in 2025 and 2026 via IPO or large M&A.

In short, this is why we believe that the gaming sector will kick off a resurgence of consumer investing within the venture capital space for the next decade. While investment in consumer still carries the risks of high customer acquisition costs, competition for attention from social media platforms, and lower than B2B exit multiples, we believe that more exits will showcase that 1) the consumer incumbents are ready to be challenged and 2) the financial health of the consumer is not a fragile as many have feared.

Side note on Valve: we did not include Valve in the lists or calculations above because this company is unlikely to sell or go public in the foreseeable future and has not (publicly) raised any funding. Valve owns gaming assets like Steam (distribution platform, ~130-140m MAUs), Counterstrike (~24m MAUs), Dota 2 (7-8m MAUs), and more. Revenue estimates for Valve are rumored to be between $7-10b per year. This company is incredibly influential in the gaming industry and has a direct relationship with hundreds of millions of consumers. If it ever sold or went IPO, that would be a momentous occasion for the industry, yet we exclude it from the above given how unlikely we believe that is at this time.

Even looking outside of the US, there are a host of companies that all have become incredibly successful and whose exits or liquidity events will meaningfully contribute to the global investment inertia around not only gaming but also consumer investing. A few notable ones include Dream Games (Turkey), Wildlife Studios (Brazil), miHoYo (China), Voodoo (France), Sky Mavis (Singapore, Konvoy portfolio company), and Mobile Premier League (India).

There are also a few gaming assets that are thriving within the corporate umbrella of larger companies. Two that come to mind are Riot Games (owned by Tencent) and Twitch (owned by Amazon). For Riot Games, the tensions between the US and China are likely to persist, which could lead to further talks around forced divestitures. A very active bidding process would emerge if Tencent had to sell Riot Games. For Twitch, it has seen an uptick in usage and monetization over the past 12-18 months, yet it fits oddly amongst Amazon’s failed gaming division and non-existent social strategy. It is possible that Amazon could sell Twitch to a better-suited buyer or private equity firm.

We believe that large gaming exits (M&A or IPO) in 2025-2026 will be the key inflection point to unleash the next wave of consumer investing for the venture capital industry. As a firm, we are excited to watch this narrative unfold and to continue our investments across both B2B and B2C within the gaming space.

Takeaway: We believe that large gaming exits (M&A or IPO) in 2025-2026 will be the key inflection point to unleash the next wave of consumer investing for the venture capital industry. The lack of investment into the consumer segment (now just 6% of the top 100 active VC dollars) creates a clear opportunity. However, we believe renewed investor interest will be driven by near term gaming exits. In the US alone, the 10 gaming unicorns account for just 10% of the 100 US consumer unicorns but command ~21% ($57bn) of the total enterprise value ($280bn) of US consumer internet unicorns. Gaming’s outsized influence combined with its near term liquidity outcomes will result in a resurgence of consumer VC investing for the next decade.

.png)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.png)

.png)

.png)

.png)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)