Newsletter

|

Mar 14, 2025

The PC gaming market faces difficult headwinds in the coming years

Copy Link

.webp)

PC gaming is as old as the video game industry itself, with some of the first games ever developed, Bertie the Brain (1950), The Nimrod (1951), and OXO (1952), created on custom computers. Personal computers, however, did not emerge until the mid-late 1970s, around the same time as arcade gaming, when home computers such as the Apple II (1977) and Commodore PET (1977) began to popularize PC gaming.

Today, PC gaming has solidified its position as the most persistent medium since the dawn of video games. There are ~1.9 billion PC gamers today, growing consistently ~3% YoY, and the PC game hardware market is over $50bn (DFC Intelligence). According to Newzoo, consumer spend on PC games (physical/digital copies of games, in-game spending, subscription services) reached $41.5bn in 2024 (+6.9% YoY).

Despite PC gaming’s strong presence and steady growth over the last few decades, this subset of the market has also experienced its own challenges in the context of the broader gaming market. Overall, the amount of time spent playing video games has decreased since the peaks seen in 2020-2021 due to the COVID-19 pandemic; the number of hours playing video games per quarter has decreased 32% from Q1 2021 to Q3 2024. For PC specifically, average play time per quarter has decreased 21% during this time period.

This week, we will assess the state of the PC gaming hardware market and how the macroeconomic environment's headwinds and tailwinds, as well as tangential technologies such as cloud gaming, artificial intelligence, and UGC, will affect its growth.

Number of PC gamers: The growth of the number of PC gamers globally has remained remarkably consistent since the late-2000s. Since 2010, the number of PC gamers has grown between 3-4% every year - with the exception of 2019-2020 (+12.4% growth due to COVID bump in the gaming market as a whole). This is despite the intermittent GPU shortages that have had trickle down affects on the PC hardware industry as a whole.

Essentially, 2 in every 3 gamers play games on a PC. Of the roughly 1.9bn PC gamers today, DFC Intelligence estimates that there are 300m high-end users (owners of high-end devices).

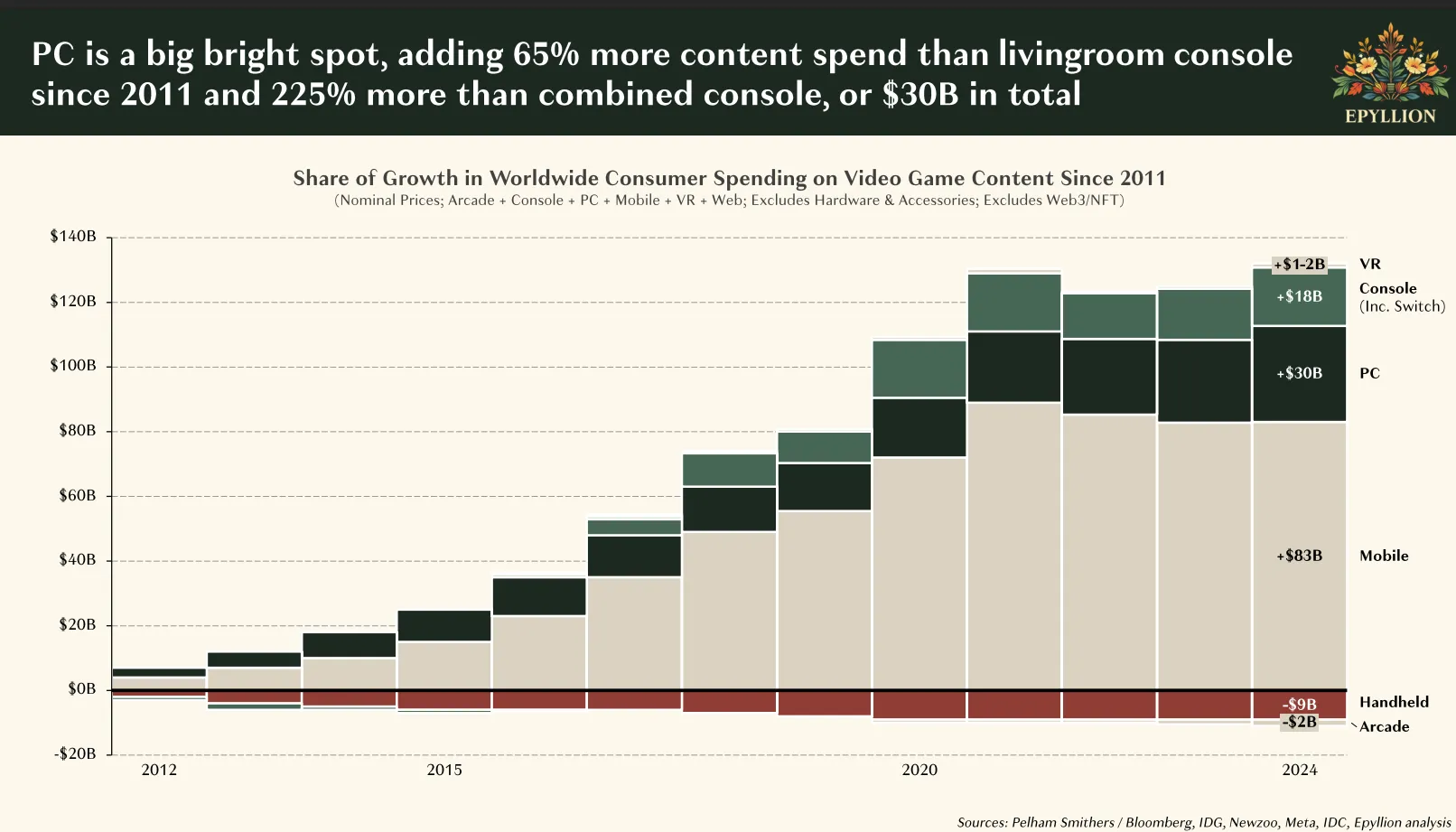

Monetizing PC gamers: The gaming PC software market has grown >$30bn since 2011, 65% more spent on content compared to that of living room consoles (Playstation, Xbox, Switch, etc). Given the player base’s consistent growth, this means that the increase in the average revenue per user is the primary driver of the medium’s growth over the last decade.

In 2004, PC’s share of non-mobile spend on gaming content was 29% (vs handheld = 22%, console = 49%). In 2024, this share of non-mobile content spend has ballooned to 53% (vs all consoles 47%).

Headwinds to Growth: Macro, Technology

While the PC market has seen steady growth in the number of gamers over the last decade, there are a number of headwinds that will have a financially negative impact on future market growth:

1) Consoles are closing the gap (technology, discovery, and distribution)

Consoles have historically provided a solid out-of-the-box experience for gamers, reducing the need for the end user to make modifications to their devices in order to play. This usually meant a tradeoff between ease of use and firepower (compute, graphics). However, the latest Playstation and Xbox models have significantly closed this gap, with models such as the PlayStation 5 Pro containing the equivalent of an NVIDIA RTX 4070 and the base model Xbox Series X containing the equivalent of an NVIDIA RTX 3060 Ti.

Console companies have also significantly removed friction for end users in solving the discovery and distribution problem through subscriptions like Xbox Game Pass and PlayStation Plus, which provide hundreds of games and curated recommendations to gamers.

2) Global manufacturing and supply chain dependencies

The global gaming GPU market was $5.5bn in 2024, with the US making up around one-third of this. Earlier this month, the US imposed a 20% tariff on Chinese imports (up from 10%). While GPU chips are often produced in Taiwan, South Korea, Vietnam, and other countries (e.g., TSMC or Samsung), sourcing and assembly can and does take place in China (TechSpot). Retailers such as Newegg, Best Buy, and Target have all confirmed the impact of these new tariffs on their inventory (PC Mag, PC Gamer). Newegg GPUs have already seen price increases ranging from $100-400 due to these tariffs. These high prices increase the barrier of entry to aspiring PC gamers. These tariffs may drive current PC gamers to other cheaper mediums or influence them to wait until the macroeconomic environment settles prices.

3) Technological innovation reducing the barrier to entry

In combination with #1 and #2, cloud gaming is offering a technological unlock that allows gamers to access high fidelity games without requiring expensive, high-end hardware (Konvoy). These cloud gaming providers are building their own infrastructure advantage; GeForce NOW works with telecommunications providers to best position their servers while Microsoft utilizes their own data centers worldwide. In fact, Microsoft believes that a majority of their growth in Xbox Game Pass subscribers will come from cloud-first gamers (compared to PC-first, console-first, or multi-device gamers). However, note that the trickle down effects of increased price of GPUs due to tariffs will affect data centers, likely increasing prices, but it is unknown how much of the increased price will be passed along to the end user.

If cloud gaming can reduce the barrier to entry for new gamers or remove the ongoing need to upgrade to the latest hardware, this ultimately suppresses the growth of gaming hardware as a whole (and hits PC hardware the heaviest, as it is typically the most expensive).

4) Increasingly difficult discovery concentrates revenue at the topIn his latest report, Matthew Ball hammers home the level of oversaturation of gaming content. To summarize, revenue has continued to consolidate to a dwindling number of games. Gamers are also buying less games; games purchased per year has declined significantly from 5.0 per MAU per year in 2020 to 3.9 in 2024 (Page 102). While this concentration of revenue may not affect overall PC gaming spend, the lack of diversification is a key risk for the growth of this market.

Despite these challenging headwinds, there are a number of tailwinds that we see contributing to the resilience of PC gaming:

1) PC-exclusive experiences

PC hardware and software enables expansive and customizable experiences beyond the “out-of-the-box” functionality that a gamer would usually get with console:

2) Developer incentives

Developers are motivated to continue to publish on PC where there is an ongoing content library advantage. Sony and Microsoft have shifted away from hardware-exclusive releases and PC-specific platforms like Steam already offer some of the best discovery in gaming (as long as you can qualify for it via Steam’s undisclosed “confidence metric”). One of the most popular engines in gaming, Unity, allows developers to publish across platforms from a single codebase (low lift, low cost).

For developers, there are also more opportunities to drive traffic toward the proper distribution platforms on PC from the web (Twitch, Youtube, X, ads on websites) or PC applications (Discord, Steam, coaching apps, etc). Redirection from a webpage or app is a more native experience on PC than it is on console or even mobile. Additionally, while PC gaming attribution is nascent today, it is technically easier for developers to attribute to the proper acquisition channel as PC attribution is not inhibited by regulation around ATT or GAID.

3) Global expansion outside of English-speaking countries

Consoles, namely Xbox, face difficult geographic adoption issues that affect the growth of these submarkets within games. For example, Xbox has faced challenges in both Asia and Europe, selling just a fraction of PlayStation’s sales.

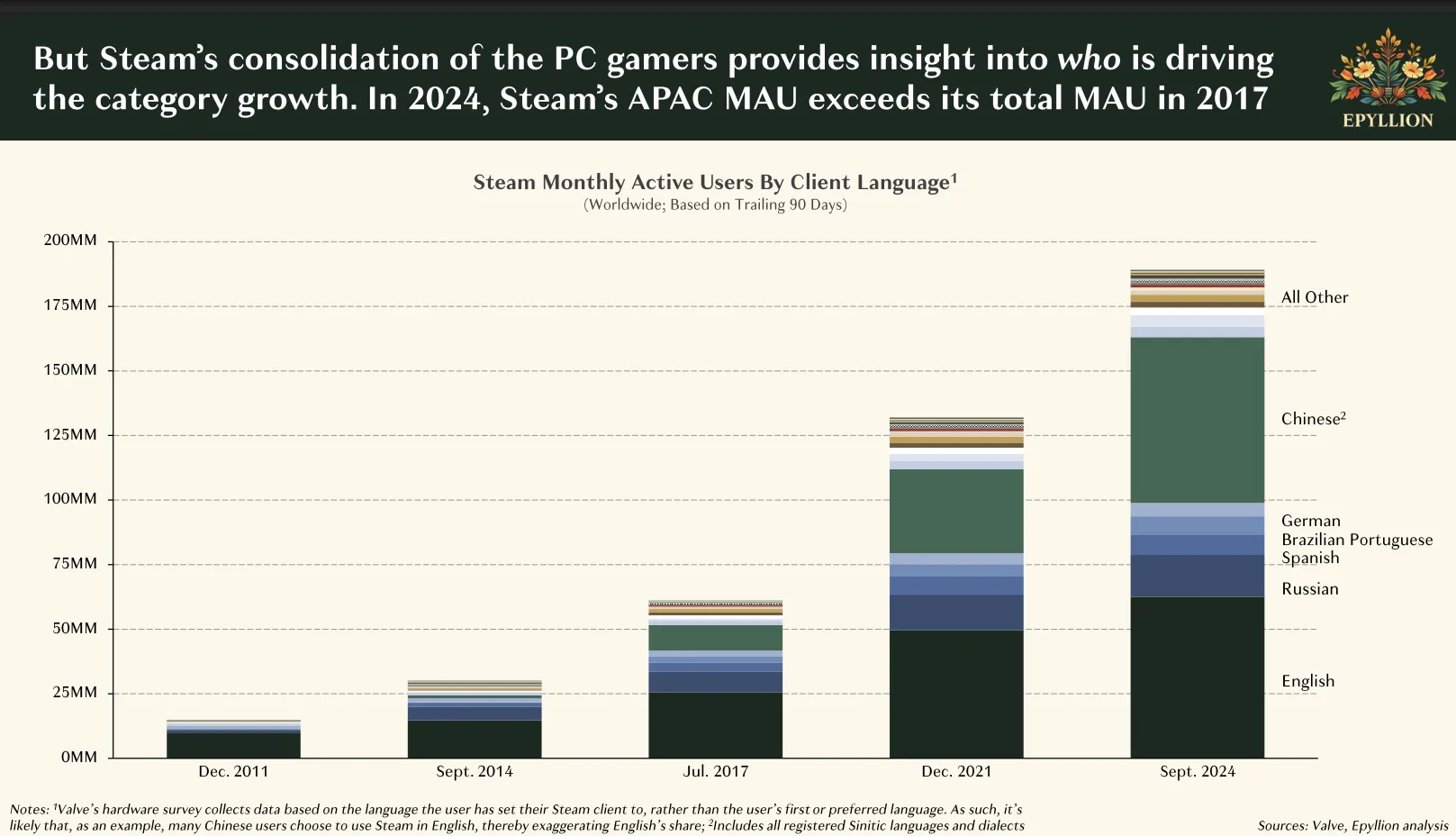

However, by usage, the PC market has seen other geographies grow even larger than the US. When using language as a proxy, Steam Monthly Active User count has seen a huge influx of users in China. Note, only 20% of China’s domestic spend goes to foreign titles.

4) The PC experience will always be more socially native

On a PC, gamers can run social apps natively (Discord) and easily access other web-native social or streaming platforms such as Twitch and YouTube. This is impossible on a console (gamers need to have Discord/Twitch/YouTube open on a separate device) or mobile (disruptive experience to switch tabs and keep the game running in the background).

5) Supply chain mitigation

It is still much too early to tell how shifts in regulation will affect the global supply chain. Companies such as Nvidia and AMD have been stockpiling inventory in US warehouses to avoid tariffs but it is unclear how much this has affected inventory and shortages (TechSpot). Additionally, over the last 5 years, secondary marketplaces such as NZXT and Jawa have emerged, offering gamers a channel to shop for pre-assembled PCs and used PCs and components. The growth of these secondary markets may be enough to anchor the size of the PC hardware market until the macroeconomic challenges are lessened.

Takeaway: The PC Gaming Market has grown over $30bn since 2011 with the Gaming PC hardware market quantified at ~$50bn today. Despite the challenging headwinds at the global manufacturing and gaming market level, and technological unlocks lowering the barrier to entry for great gameplay, we believe that both the gaming PC market and the gaming PC hardware market will remain resilient over the next few years. This market resilience and growth will be anchored by global expansion outside of English-speaking countries, a desire for more socially native experience by gamers, and ongoing motivation for developers to continue to publish for PC.

.png)

.png)

.png)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)